Understanding Post Office Interest Rates: Tables and Calculation Methods

Dear readers, are you curious about understanding the interest rates of post offices? You have come to the right place then. Knowing about the interest rates of post offices, their methods, their tables and calculations, it all can be beneficial for you and your financial planning for long term as well as your investments and savings for the same.

Normally, a post office will offer a variety of schemes to invest in that can provide investors with great returns and benefits for the long term. These investments can be proved to be a boon for their finances and all of these can be fulfilled with different goals. In this blog, we will look into different methods for calculating the rate of interest of post offices to know exactly where our investments are going. Lets dive right in.

A Post Office

A post office is basically a government organisation that deals with the service of mailing a letter or a postcard from one place to another. It is also included in the selling of stamps and other packaging items.

Along with this, a post office also provides a Post Office Investment Saving Scheme that is just like any other investment option that could provide guaranteed returns because of being a governmental organization or being backed by a government.

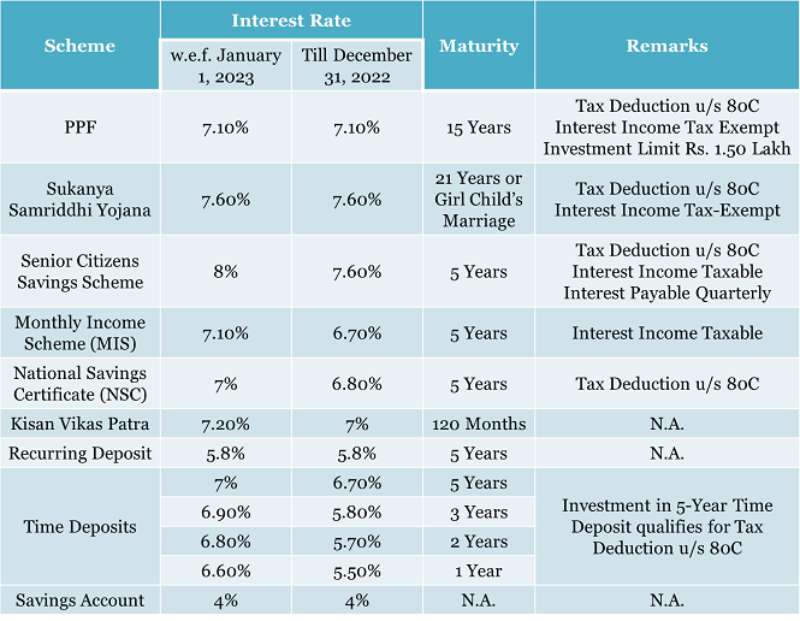

Post Office Interest Rate Tables

A post office interest rate table is a table that carries data about the particular interest rate according to the scheme and the duration or tenure of your investments. The latest table would provide you with the name of schemes and their tenure along with the interest rate levied on each.

It is of utmost importance that interested investors and other common public keep themselves updated about these tables to make better decisions for themselves even in the future.

You should also consider reading:- Free Online Courses With Certificates In India

Calculation Methods

It is important for users to know about the calculation methods of interest rates to estimate their growth and make decisions accordingly. Any calculation for any interest rates is always the two methods :

Simple Interest

Simple Interest is the most common one where the product of the amount of principal or money invested, the rate of interest and the return is divided by 100.

Compound Interest

Compound interest is of the main use here while calculating the interest rate of post offices. In this type of interest, all you have to do is the use the formula

Maturity Value= P(1 + r/4) (nx4)

Where,

P is the Principal amount,

R is the rate of interest, &

N is the number of years

(4 is used because it is calculated quarterly)

It is important to take note of the fact that the interest is calculated quarterly for all post office savings or investment schemes but paid annually.

You may also like to read - Ajio rs 500 off on 1250 coupon code

Factors Affecting Post Office Interest Rates

Inflation is the biggest factor that can affect the rate of interest of post offices. They can hamper the money power and fluctuate the overall rate in the market.

Government Policies also play a major role in influencing the post office interest rates. The policies of the Ministry of Finance and their changes in monetary policies can affect the rate of interest.

Market Stability is another point that can cause the rate of interest of post offices to fluctuate along with other variable factors such as the environment of the market.

You may also like to read - How Late Is The Closest Grocery Store Open

Types of Post Office Saving Scheme

According to latest research, a few of the present-day schemes of post office are listed below :

Post Office Savings Account (SB)

Like any other saving account, POSB is also a basic saving account having a minimal normal interest rate of 4%.National Savings Recurring Deposit Account (RD)

In a recurring deposit account, the account holder has to deposit a certain fixed amount of amount in a span of a few months with an interest of 6.7%.Senior Citizens Savings Scheme Account (SCSS)

Particularly for senior citizens, this scheme provides better interest rates for their benefit of about 8.2% (as of march 2024)Public Provident Fund Account (PPF )

It is a long-term savings scheme for a slow and steady and secure future. This account has an interest rate of 7.1% with a 15-year tenure.

Also Read - How To Check Delhi Metro Card Balance

Checking and Comparing Interest Rates

Always be up to date to benefit from the best scheme that shows up.

Always compare the Interest rates of various schemes and then make an informed decision.

Always check for your eligibility before thinking of any investments. For example, SSA is only for girl children and KVP is particularly for Kisan.

Other financial institutes also provide investment opportunities so checking those could be beneficial for any investor.

Conclusion

As we reach the end of today blog, there are a few things we would like to remind the readers. Always check with the head of your nearest post office or your financial advisor before you step into anything. Moreover, it is always better to know and understand everything about your investments before actually investing. With proper guidance and knowledge, individuals can make an educated and informed decision about their investment to achieve a financial goal, whether short-term or long-term.

Always review tables and charts about the new schemes and investment options and keep yourself up to date about everything going on around your field of interest to catch the best opportunity at the earliest. This will help you reach your goals in a shorter time. Couponscurry.com will continue to bring such articles that would help you in your daily life. Stay tuned, and happy investing!

Consider Reading:-

- GoPro Hero 13 Black Hands-On Review: Price, Release Date, Features, and Legit Kit

- Shoe Size Chart India

- Best Dry Fruits Brand In India

- Best Trimmers For Men Under 1000

Play Anywhere, Anytime with App

Play Anywhere, Anytime wi ...

Get up to 75% OFF on Ethical Beauty Products

Get up to 75% OFF on Ethi ...

Sports Nutrition – Get up to 67% OFF on Your Purchase

Sports Nutrition – Get ...

1 Plus 1 Offer – Get Two Pizza At Rs.99 Each

1 Plus 1 Offer – Get Tw ...

Get 20% Discount on LUX PARKER Men Regular Fit Undershirt.

Get 20% Discount on LUX P ...